A new layer of software has crept onto every bank desk — and it is changing how the work actually gets done.

Call it a research co-pilot, an underwriting shortcut, or simply a digital analyst. The tools are in front-line workflows at big banks, wealth managers, and trading floors. The benefits are easy to see: faster note-writing, instant data pulls, smoother client conversations. But adoption is moving quickly, and that speed is exposing practical, legal and market risks that are forcing firms to slow down and rethink.

Why this matters now

This feels less like a shiny feature and more like the waves that followed spreadsheets or electronic trading. In the near term people are squeezing productivity out of existing teams; a bit further out, new operational risks show up that regulators never had to consider a decade ago.

- Productivity: Pilots report roughly 20–40% time savings on routine drafting and data extraction, according to industry surveys.

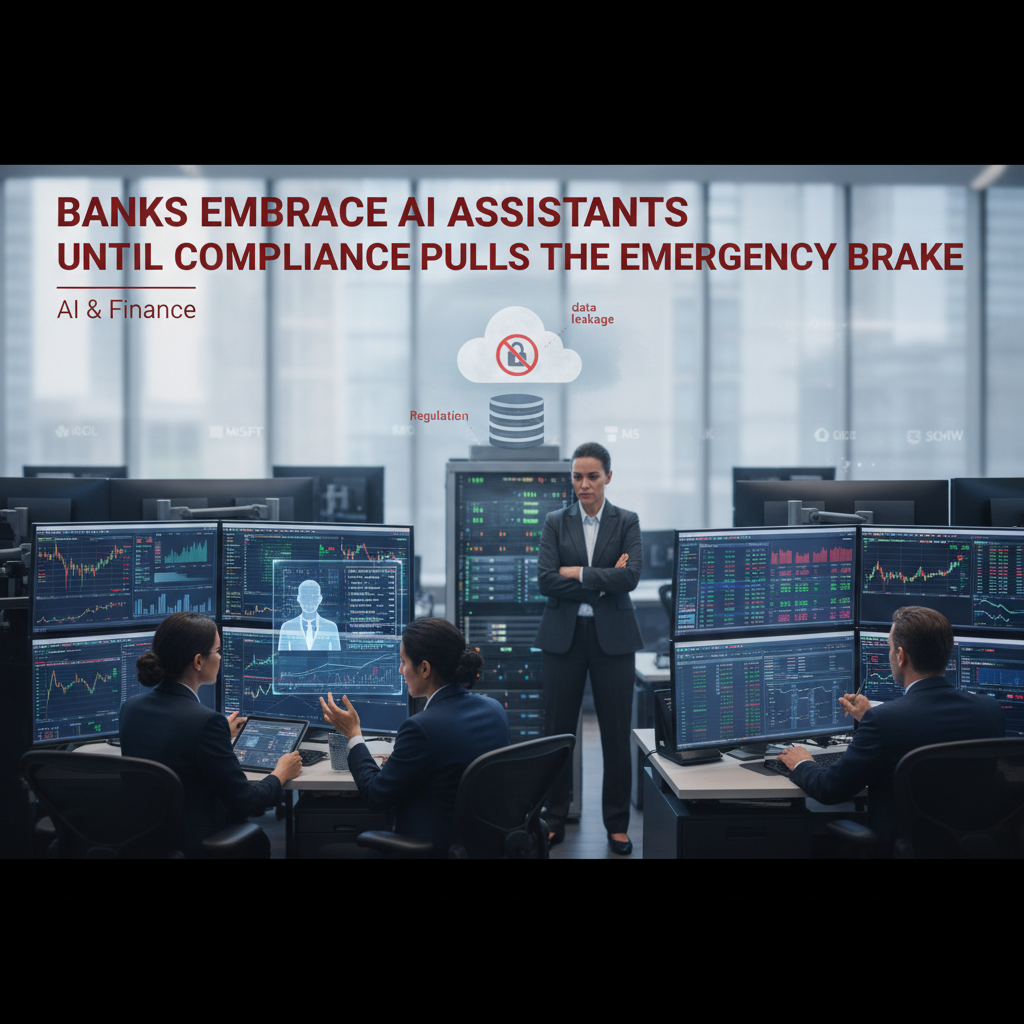

- Concentration risk: Deployments often rely on a small set of cloud and model providers, which creates vendor lock-in and a single point of failure.

- Compliance complexity: Chat logs, prompt versions, and model updates produce audit trails that legacy compliance systems struggle to interpret.

Real-world frictions

The models make mistakes that look authoritative. They can invent a source, misread a contract clause, or spit out numbers that seem plausible at a glance. Those aren’t just awkward errors — they can produce misleading advice, warped risk signals, or trigger regulatory attention.

Data leakage is another acute worry. Pushing proprietary spreadsheets, client lists, or trade plans into third-party models without ironclad controls invites intellectual property loss and, worse, information that could move markets.

Regulators are catching up — faster than many expected

Agencies are moving. Expect guidance from the SEC and FINRA on recordkeeping, model validation, and vendor oversight. The likely enforcement theme: failed controls, not the mere fact a firm used a model. Think of it as accounting and disclosure rules trying to map onto a new kind of black box.

Where banks are putting money

- Stronger model governance: tougher validation, continuous monitoring, and formal red‑teaming of outputs.

- Private deployments: on-prem or private-cloud setups to keep sensitive data off public APIs.

- Explainability tooling: richer logs, prompt versioning, and provenance metadata so auditors have something to look at.

A few strategic takeaways

- The competitive gap won’t be who has AI, it will be who runs it safely. Firms that get governance right can scale fast without signing up for headline risk.

- Vendors that offer private models and built-in compliance tooling will command a premium. Expect big cloud providers and specialized fintechs to compete hard for that trust.

- Talent is shifting. Compliance engineers, prompt auditors, and AI-ops specialists are becoming as important as quants and traders.

A cautious view

This is not an existential threat to markets. Historical precedents — program trading, algo markets — eventually settled into regulated practice. Still, the near-term is messy. Treating these tools like invisible plumbing — quick to install and then ignored — will cost firms. Treating them like a new class of operational risk, with policies and controls, is the path to capturing the upside without the headlines.

What to watch next

- SEC and FINRA updates on AI use in advisory work and trade decisioning.

- Big banks publishing AI governance playbooks as signaling to the market.

- Vendors rolling out private models with auditable trails and compliance integrations.

If you trade or advise, expect a season of careful experiments, louder compliance teams, and a competition to prove generative models can be both useful and safe.