Market context

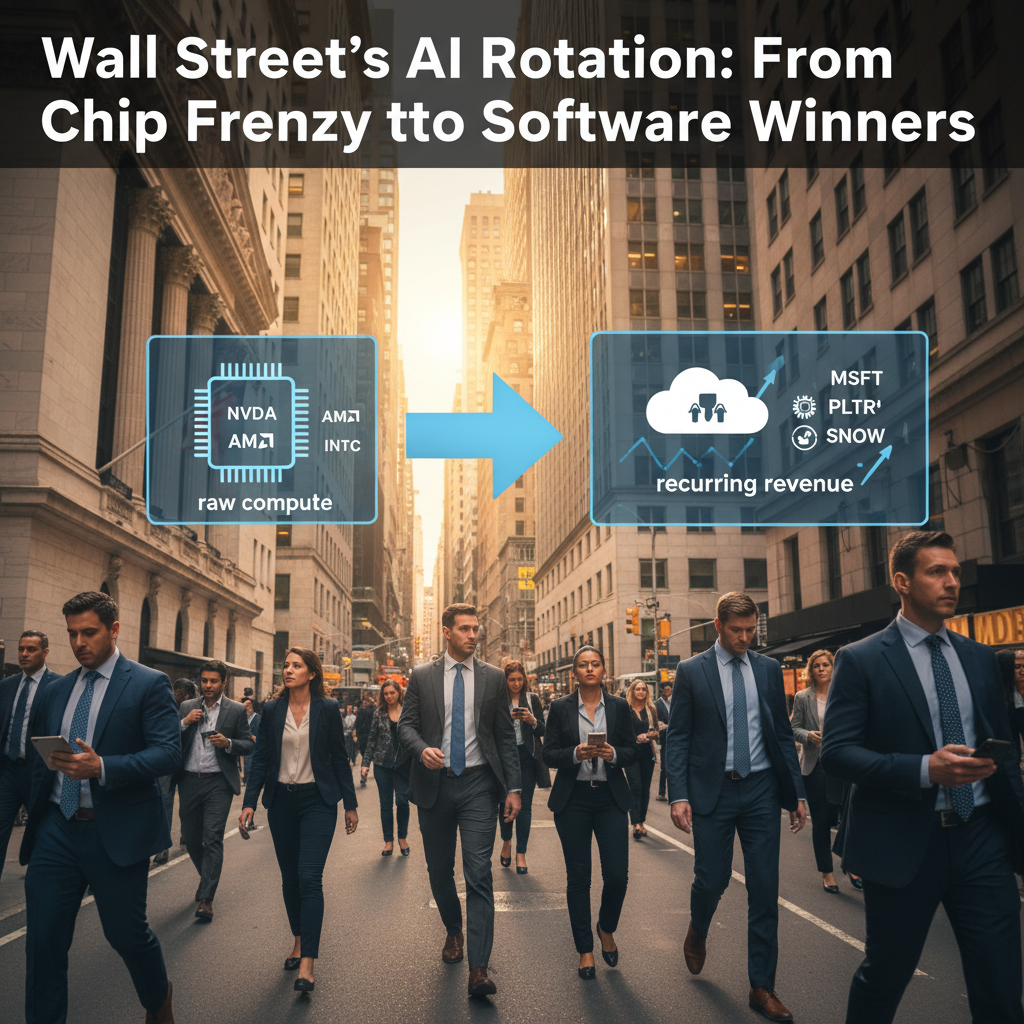

The simple story that’s dominated recent years — GPUs power AI, and Nvidia sits near the center of that — still holds at a high level. But under the surface a quieter rotation is happening. After a hardware-led sprint, investors are starting to prize software and cloud firms for what they offer: higher margins, recurring revenue, and customer stickiness. That changes the risk-return mix in an important way.

Why the rotation makes sense now

- Margins and predictability. Software and cloud companies tend to turn AI interest into subscriptions and services revenue — steadier cash flows than a speculative hardware boom.

- Competition and commoditization. GPUs are becoming crowded and custom silicon is spreading; hardware margins look more exposed. Software scales without the same capex drag.

- Policy and supply noise. Export rules, geopolitical supply chains and lumpy capex cycles make hardware a noisier bet. Software spreads that operational risk across customers and regions.

What’s interesting is how these forces interact. Software isn’t immune to churn or competition; hardware won’t disappear. Still, the relative appeal has shifted.

Names to watch (and why)

- Microsoft (MSFT): A big cloud AI play with deep platform hooks. Enterprises are more likely to adopt AI through hosted services than by standing up their own racks — and Microsoft sits squarely in that path.

- Nvidia (NVDA): Still central to compute demand. But investors need to account for more competition, cyclical capacity, and valuations that already bake in very high growth.

- Palantir (PLTR) and C3.ai (AI): Two different software-first tests. High-margin potential is real, but execution and sales motion will determine whether AI dollars become durable revenue.

- Snowflake (SNOW): Data and models are symbiotic. Firms that control clean, shareable datasets and smooth model deployment can capture disproportionate value.

None of these are slam-dunks. Each has its own execution gap and timing risk.

A counterpoint worth holding

Chips are not going away. Compute demand is compounding; data centers will still need hardware. If you expect multi-year growth in model sizes and compute intensity, owning select hardware names makes sense. The point is not an either-or switch but a rebalancing of weights aligned with timing and risk tolerance.

Tactical signals for investors

- Listen to enterprise AI spend in earnings calls and guidance, not just marketing headlines.

- Watch cloud gross margins and contract lengths; multi-year deals are a stronger signal than pilots.

- Track server bookings and capex commentary for whether hardware demand is genuinely growing or merely lumpy.

- Favor companies that convert pilots into recurring contracts — that’s where economics start to show up.

Takeaway

We’re moving past single-name mania into a more nuanced phase. Think of it a bit like the late 1990s: hardware opened the door, but long-term profits tended to land with the software firms that learned to charge for real usefulness rather than raw horsepower. That does not mean dumping chips — it means calibrating exposure and focusing on durable economic moats.